Frescobaldi: Italian producers cut prices, but shelf prices rise – U.S. trade must do its part

January 30, 2026 (Rome, Italy) — For the fifth consecutive year, overall wine consumption in the United States has declined. The U.S. remains the world’s largest wine market, with an estimated retail value of around USD 60 billion per year, including approximately USD 8 billion generated by Italian wines alone.

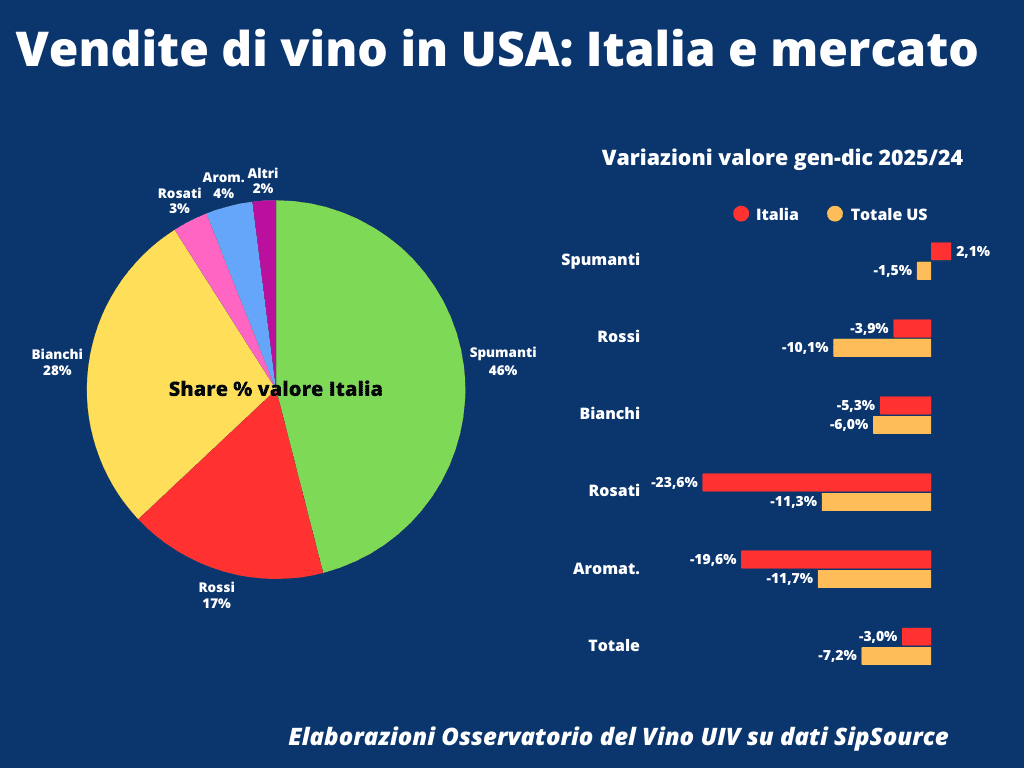

According to data from the Wine Observatory of Unione Italiana Vini (UIV) based on Sipsource, total wine sales across supermarkets, wine shops, restaurants and on-trade channels fell by 8.8% in volume and 7.2% in value.

Italy also closed 2025 with negative results, but performed better than the market average, recording a decline of 5.2% in volume and 3% in value, compared to an overall market that was strongly affected by the crisis of U.S. domestic wines, which posted volume losses close to 10%.

The contraction of Italian wines was mainly mitigated by the strong performance of Prosecco (+3.7% in value), as well as by renowned red appellations such as Chianti Classico and Brunello di Montalcino. All other major PDOs experienced declines. Despite this, Italy remains the leading country in imported wine consumption in the U.S., in a year that also marked a new leadership of the sparkling wine category, both in volume and value, with 47.5% market share for Italian sparkling wines compared to 46% for France.

Lamberto Frescobaldi, President of Unione Italiana Vini, commented:

“Over the last four years, wine consumption in the U.S. has fallen by about 20%, while Italian wines have declined by around 12%. In a market already weakened by lower purchasing power, the tariff environment is even more impactful, especially now that retail prices are rising. In December we recorded a year-on-year price increase of around 4%, despite the fact that Italian producers reduced their price lists by an average of 10% over the last six months.

At this stage, everyone must do their part to keep demand alive. Producers are doing theirs, while the U.S. trade much less so, and this risks becoming a boomerang for the entire system.

The United States remains an irreplaceable market for Italian wine, but with exports expected to close 2025 down 9% in value, we must accelerate new free-trade agreements in response to protectionist trends. Every new partnership is both an opportunity and a responsibility, starting with Mercosur and India.”

According to the UIV Observatory based on Sipsource, which tracks U.S. distributor warehouse depletions, Italian sparkling wines are the only category showing growth in commercial value (+2.1%). Red wines limit their losses to -3.9%, compared with -10.1% for the overall red category, while white wines decline by 5.3%. Both rosé and aromatised wines register drops of around 20 points.

In terms of spending composition, sparkling wines now account for 40% of total U.S. expenditure on Italian bottles, followed by whites at 28%, reds at 17%, aromatised wines at 4% and rosés at 3%. Geographically, consumption of Italian wines is led by the South, which represents 48% of the total, followed by the Northeast with 18%, the West with 17% and the Midwest with 16%.

Among competitors, France managed to keep the value of its sales almost stable year on year at -0.2%, supported mainly by white wines and Champagne, while Spain declined by 4.7%. Among New World producers, New Zealand, a leader in white wines, limited losses to -2.9%, whereas all others, from Australia to Chile and Argentina, posted double-digit declines. U.S. wines, which represent 67% of total U.S. wine consumption in value terms, fell by 8.6%.

UIV – Unione italiana vini (https://unioneitalianavini.it/) is the most influential association representing Italian wine companies: more than 800 members, accounting for more than 50% of the total turnover of wine in Italy and more than 85% of the export turnover of Italian wine.