Unless otherwise noted, all trends below are for dollar sales within Nielsen U.S. off-premise channels for the one-week period ending 8/15/20 compared to the same week in 2019. We continue to remind our readers that we are only measuring some specific off premise channels, and that the impact of the health crisis on sales is uneven across companies in the alcohol industry.

Unless otherwise noted, all trends below are for dollar sales within Nielsen U.S. off-premise channels for the one-week period ending 8/15/20 compared to the same week in 2019. We continue to remind our readers that we are only measuring some specific off premise channels, and that the impact of the health crisis on sales is uneven across companies in the alcohol industry.

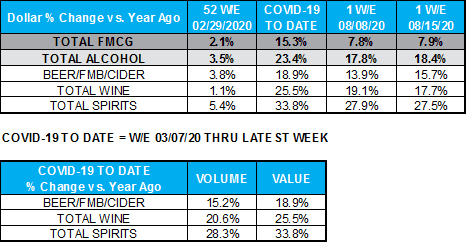

The year-over-year growth rate for total off-premise alcohol dollar sales within Nielsen measured channels was +18.4% (now +23.4% for the entire 24-week pandemic period).

- Spirits continue to lead growth, up 27.5%.

- Wine grew 17.7% in dollar sales.

- Beer/FMB/cider growth was at +15.7%.

In the words of Danelle Kosmal, Vice President of Beverage Alcohol at Nielsen:

“Canned alcoholic beverages have received a lot of attention, and for good reason. Compared to last year, all within off-premise channels, canned beer/FMB/cider is up 25% during the pandemic, and canned spirits are +140%. And as restaurants began to expand on ideas like canned wine gardens, it will be interesting to see if this will further normalize the idea of cans and other alternative packaging for wine and even ready-to-drink cocktails.”

ON PREMISE

NOTE: this section is focused on the on-premise (bar, restaurant, taproom, etc. space), from the Nielsen CGA team. Everything else in this report is focused on the off-premise (retail…grocery store, liquor stores, etc.) space.

Visitation to bars/restaurants for eating occasions slightly increased in the previous two weeks: 46% have been out to eat in the past two weeks and 14% have been out for a drink.

We see an increase in the percentage eating out particularly in Florida, suggesting there has been a positive response to the stricter guidelines placed on venues.

Mid-value drinks/brands are the most frequently ordered in bars/restaurants (50%) and 7/10 consumers are doing this as frequently as pre COVID-19.

On the flip side, 35% of consumers ordered a premium drink in the last two weeks, but 50% of those consumers said they are doing this more than pre Covid-19. This shows a group of consumers are treating themselves within the On Premise market.

The number of consumers going out at least 3 times in the last 2 weeks continues to increase, showing frequent visitation is still seeing improvement and those who are going out are growing confidence.

BEER/FMB/CIDER: OFF PREMISE

For COVID YTD (first week of March through 8/15/20), beer/FMB/cider is up 18.9% in Nielsen off premise channels. Off premise growth rates have slowed some since the beginning of June, which are up 15.9% in off premise channels for the total category, and up 8.6% for core beer (excluding “beyond beer” segments). For the latest week, beer/FMB/cider grew 15.7% in off premise dollar sales.

For the latest week in off premise sales, all segments are growing, with the exception of below premium, which is down slightly (-0.3%) compared to the same week last year. Premium light brands are up 6.4%, with all three premium light brands among the top 15 growth brands for the week.

Hard seltzers led growth, up 123% for the latest week compared to last year. As a reminder, there are very tough comps from August 2019 for hard seltzer, so the continued triple-digit growth for hard seltzers is one of so many signs that hard seltzers will not slow down. For COVID weeks (beginning first week of March), hard seltzers accounted for 9.2% of total category dollars in off premise. Hard seltzer share has accelerated during the summer months, and now accounts for 10.5% of category dollars for the latest 11 weeks ending 8/15/20. Other strong segments for the week included hard tea +38%, super premium +22%, craft +14.4%, cider +11.9%, and non-alcoholic beer +40%. Mexican imports had its strongest week in a while, up 11.2%.

With the improvement in craft beer trends in off premise, particularly during the past several weeks, we dug into some of the specific styles that are driving those growth trends. Total craft growth for COVID year to date (week ending 3/7/20 through 8/15/20) is 15.8% in Nielsen off premise channels. IPAs (+26.5%) continue to outpace total craft growth in off premise, and are still by far the largest style in craft beer, accounting for 41% of off premise craft dollars for COVID year to date. This is up from 37% for that same time period last year. However, most of that share growth was driven by hazy IPAs and imperial/double/triple IPAs. If we were to remove hazy and double/triple IPAs from the scope, IPAs would be up 18% in dollar growth, and account for 26.8% of craft off premise dollars, up only 0.5 share points from last year. Hazy styles now account for 7.0% of craft off premise dollars, and are up 78% in dollar sales for the COVID YTD time period compared to last year. Other craft beer styles that are leading growth in off premise during COVID weeks include American wheat ales (+113%), sour ales (+61.3%) and non-alcoholic craft beers (+176%).

WINE: OFF PREMISE

In Nielsen off premise channels, wine is up 25.5% in dollar growth for COVID weeks, and up 17.7% for the latest week ending 8/15/20.

Sparkling wine growth (+35.5%) continues to outpace growth of table wine (+13.5%), with French champagne leading (+72.3%).

Wine-based cocktails had triple-digit growth in the latest week, up 109% compared to the same week last year.

Within table wine, all price tiers are growing, with the exception of value wines (<$4), which were down 5.3% in off premise for the latest week. All price tiers $11 and higher are experiencing strong double-growth in off premise channels for the latest week.

SPIRITS: OFF PREMISE

In Nielsen off premise channels, total spirits are up 33.8% for the COVID YTD time period, and up 27.5% for the latest week.

For the latest week, ready-to-drink cocktails lead growth, up 113%, followed by tequila (+61.2%), cognac (+59.8%), cordials (32.2%) and whiskey (+25.6%).

Small spirits sizes continue to bounce back in growth compared to early COVID weeks, with 100 ml bottles up 33.9% and 50 ml up 22.9% for the latest week in off premise channels.

PACKAGING: CANS

In beer/FMB/cider, cans account for 64% of category dollars, and are growing in dollar sales, up 25% for COVID weeks (beginning the first week of March) compared to the same time period last year. Slim cans in particular are leading growth in the category, up 107% for COVID weeks compared to last year. Slim cans currently account for 20.4% of can dollars in beer, up from 13% in pre-COVID time periods.

In wine and spirits, cans account for a very small percentage of dollar sales; however, with the growth of canned wines and canned ready-to-drink cocktails, spritzers and seltzers, they are becoming increasingly more important and popular.

In spirits, cans were nearing triple-digit growth even prior to COVID (+88%), and that growth has accelerated during COVID (+140%) in Nielsen off premise channels. Cans account for an extremely small portion of total off premise spirit sales (1.2%), but that has nearly doubled since pre-COVID time periods.

Wine is the one category where can growth has slowed during COVID. While there has been a lot of recent discussion around canned wine growth, off premise canned wine sales for COVID year to date (+57%) actually lag growth rates for pre-COVID time periods (71%). That said, share of canned wine is increasing, with cans accounting for 1.1% of total category dollars in wine during COVID weeks, up from 0.8% in pre-COVID time periods in off premise channels. Historically, canned wine has held a stronger presence in off premise compared to on premise.

Overview: Nielsen COVID-19 insights and analysis

- Nielsen.com: How Americans are Shopping During COVID-19

- Nielsen.com: Rebalancing the ‘COVID-19 Effect’ on Alcohol Sales

- Nielsen CGA: COVID-19: Measuring the On Premise Impact